In what appears to be the latest move towards damage control for Obamacare, the administration will once again be promising everyone that “if you like your plan you can keep it” for at least another year. This election season maneuver is designed to alleviate concerns from small businesses, many of whom will experience rate shock and forced benefit changes, to potentially avoid the new rules imposed under the law.

Many small businesses, those defined as having less than 50 full time eligible employees, took advantage of a small loophole in the law that allowed them to renew their current employer-sponsored insurance plans effective December 1, 2013. Renewing their policies in an off-cycle time period gave businesses the opportunity to postpone meeting the strict requirements of Obamacare until December 1, 2014. Since insurers must send out cancellation notices 90 days in advance, this would mean that over 17 million employees who receive benefits from their employer would receive cancellation notices around September 1st, only weeks before voters go to the polls.

The false promotion of “sub-par” plans

According to President Obama, the reason for eliminating consumer choice was that the plans were “bad insurance”. The reality is that, in the employer market, most (if not all) of the Essential Health Benefits along with the Minimum Essential Coverage requirements, have been in employer sponsored insurance plans for years. According to a report from HHS in November of 2011 “the overwhelming majority of employer-sponsored insurance (ESI) plans meets and exceeds an actuarial value (AV) of 60 percent.” In fact, less than 2% of people covered by ESI didn’t meet the 60% requirement set forth in Obamacare. This means that only 2.6 million to 3.2 million are impacted.

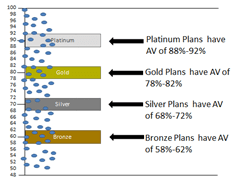

Actuarial value is the amount of medical services covered, on average, by an insurance plan. Prior to 2014 insurance companies could offer plans that had any actuarial value. Now, there are strict guidelines Obamacare uses for determining what plans are good insurance versus what plans are bad insurance and any plans created from 2014 and forward must fall into the so-called “metal tiers”. Insurers are hamstrung in the individual and small group market and are only allowed to offer insurance plans that fall into narrow actuarial value bands. These metals – Bronze, Silver, Gold, or Platinum – have actuarial value of 60%, 70%, 80%, or 90% respectively. Variation from these figures is +/-2%. Here is what plans looked like in 2013.

*The blue dots represent insurance plans.

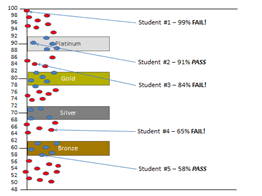

Because Obamacare only allows plans within the strict actuarial value ranges, any small employer who is looking to change plans will now have limited choices. In most cases small employers are already offering an excellent benefits package but will now be forced into a plan that meets the government definition of “good insurance”. All other plans are eliminated and considered “sub-par”.

Red dots are plans that Obamacare calls “sub-par”

These plans are cancelled under the law

A great analogy is comparing actuarial values to school grades. Bob Graboyes, of The Mercatus Center at George Mason University, and I wrote a piece on this a few months ago. To illustrate: let’s say a school has 5 students. Student #1 is set to be valedictorian and has a 99% average. Student #2 has a 91%, Student #3 has an 84%, Student #4 has a 65%, and Student #5 has a 58%. Because these students don’t fall into the strict grading scale defined by Obamacare, the student who has a 99% is set to fail. That’s because he falls outside the “approved” range. In fact, all students with grades between 93% and 100% will fail. The same happens to the student with an 84%. But student #2 at 91% passes! Even the underachiever with a 58% passes. This is the reason why people are losing their plans.

Rate shock!

The big elephant in the room for small business owners is high costs to insure people. The promise of every family saving $2500 wasn’t something employers ever believed would happen. But they also didn’t anticipate the significant increase in premiums they are about to see due to community rating and narrow age bands. Traditional underwriting in any risk product revolves around the potential exposure to claims. Health insurance has always been underwritten by insurance company actuaries working to determine the risk of individuals based on their medical conditions, age, gender, and other criteria. In determining insurance rates, the actuaries could increase or decrease pricing to a company (not an individual employee) based on the health status of the employees. According to CMS, over 65% of small businesses will see increases in their premiums due to the new requirements under Obamacare. This is because the majority of employers who offer insurance are in relatively good health. Now many employers will face significant rate increases because actuaries can’t adjust rates for any risk factors except age, location, and tobacco use status.

Tough to swallow

Rate shock and losing the plans employers like is already happening. Some companies that have grandfathered (GF) plans are already feeling the pinch. I have a client that is GF with an April renewal. They offer two plans. One has an AV of 76% and the other is 85%. They can’t make any benefit changes or they will face a host of new, expensive Obamacare requirements. Their renewal rates include a 27.4% increase, a big pill to swallow. However, the alternative is to change their plan designs to fall into the metallic tiers, fall under community rating, and more. The premiums would increase by 45%-70% depending on the insurance company they choose. Now we’re talking about a huge suppository.

The President’s blessing that people can keep their current insurance plan is simply a way to help his party as they head into election season. Not a single Democrat wants to head back home to hear about businesses cutting employment, raising premium contributions on employees, or simply dropping their insurance plans. Taking this action now will help stave off some of this potential risk.

Republicans should keep their pressure on Obamacare and the complete disaster this will have no matter when it is fully implemented. Allowing the President to unilaterally push back deadlines without calling him out isn’t an option.

After all, elections have consequences.