The launch of Obamacare’s online insurance exchanges has been such an operational trainwreck that even the White House Press Secretary, the DNC chair and boosters like Ezra Klein have had to acknowledge that it’s been a disaster. Industry observers are mystified.

But the technology is just the surface problem; the larger issue is that the entire economics of the insurance sold on the exchanges – always tenuous at best – is threatened by the combination of poor functionality, intrusiveness and sticker shock, leading not only critics like Phil Klein and Megan McArdle but even supporters like Jonathan Chait to argue that the Obama Administration should delay portions of the law to salvage it (more on that here) – a result that would be deeply ironic and humiliating to the Administration, after President Obama just spent a month beating back furious Republican efforts to force delays in the launching of the exchanges and the individual mandate. But suggestions for delaying the mandate without going hat in hand to an irate Republican Congress ignore an important reality: any delay of the individual mandate would risk lawsuits in which the legal positions the Obama Administration took to defend the mandate could come back to handcuff its freedom of action.

How Universal Insurance Is Designed To Work

Let’s recall that the heart of Obamacare is not the exchanges and it’s not the subsidies to help people buy policies they can afford; it’s three rules designed to (1) compel both insurers and individuals to do business with each other, so that everyone gets covered, and (2) do so without bankrupting the insurers or sending the cost of subsidizing policies sky-high. The problem is pooling of risk: if only the sick and the old buy policies, the insurers will have to charge them as much for their policies as it would cost to just pay for their care, which defeats the entire point of insurance. You need some people paying in who are not already making claims, so you need to entice young, healthy people to buy insurance that effectively subsidizes the rest.

The first rule is guaranteed issue: insurers cannot turn away people with pre-existing conditions. This alone drives up the insurers’ costs, which is why healthy people need to be compelled to buy their policies to keep the system solvent.

The second is community rating, which – to simplify – controls the premiums that can be charged by requiring insurers to price policies by looking at the risk of the entire pool rather than just the specific actuarial characteristics (including pre-existing conditions) of the individual. Community rating doesn’t control the premiums of the overall pool, it just shifts and socializes that cost onto young, healthy policyholders.

The third is the individual mandate, which provides compulsion of the individual in the form of what the Supreme Court characterized as a tax. Without the mandate, healthy people may rationally choose not to buy overpriced insurance priced at community-rated premiums, leaving the insurers forced to cover a small, self-selected pool of the sick and the elderly.

Legal Trouble

Hypothetically, let’s say the Administration decided to keep the exchanges open, requiring insurers to keep providing guaranteed-issue policies priced at community-rated terms, but announced that it would delay enforcing the individual mandate. There’s no way the Administration could or would keep the exchanges open otherwise, since the whole economic benefit of the project for people in immediate need of coverage would be gone, and indeed many would simply be denied coverage.

But that would be a disaster for insurers, roped into the guaranteed-issue mandate but unable to compel healthy people to buy the policies that make guaranteed-issue even remotely economically feasible. They would simply hemorrhage money. And because businesses don’t exist to hemorrhage money and the statute doesn’t authorize a suspension of the mandate, some insurer would likely challenge any delay in court.

And that’s where the Administration could be hoist on the petard of its own legal arguments. When Obamacare went to the Supreme Court, one of the issues presented was “severability”: that is, if the Court struck down the individual mandate, would it also strike down the entire statute. The Solicitor General’s brief on behalf of the Administration said no – but argued that if the mandate was struck down, the Court would have to also strike the guaranteed issue and community rating provisions because Congress would not have authorized them without the mandate. The key passages are pretty unambiguous:

The minimum coverage provision [i.e., the individual mandate] is essential to ensuring that the Act’s 2014 guaranteed-issue and community-rating reforms advance Congress’s goals… As Congress expressly found (and as experience in the States confirmed), those provisions would create an adverse selection cascade without a minimum coverage provision, because healthy individuals would defer obtaining insurance until they needed health care, leaving an insurance pool skewed toward the unhealthy.

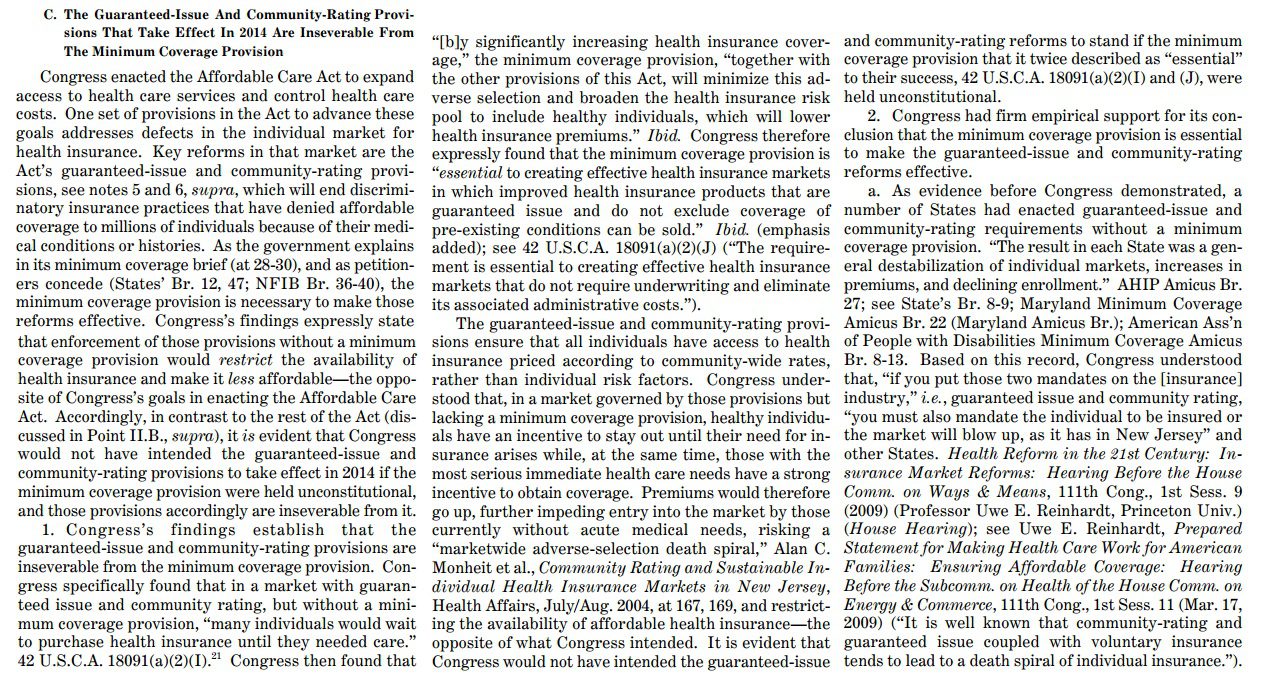

Here’s a longer excerpt of the SG’s brief:

(Click to read)

The brief goes on to detail Congress’ “empirical support” from the experience of states that have experimented with community rating and guaranteed issue without a mandate, with bad results.

It’s impossible to predict how the courts would rule on a legal challenge to delaying the mandate without delaying guaranteed issue and community rating. But the Administration’s own legal arguments would provide a powerful argument for insurers that Congress never intended these provisions of the statute to be enforced against them while the mandate was not in effect. And the economic arguments in that brief illustrate why the Administration may be hesitant to do so for reasons going beyond politics. So, extricating itself from enforcing the mandate until the exchanges can be brought up to speed may prove easier said than done.